Now you know why OpenAI is transitioning to a public benefit company…

Sharp-eyed netizens discovered that OpenAI actually lost $11.5 billion last quarter!

The key point here is that this isn’t hearsay from some media outlet; it was revealed directly by OpenAI’s largest backer—Microsoft itself.

What’s going on? Did the little brother get so busy building apps for Apple that he really annoyed his boss??

Let’s take a look at what exactly happened.

Microsoft Takes a $3.1 Billion Hit Due to “Little Brother’s” Losses

Microsoft has undoubtedly reaped massive profits in this AI wave.

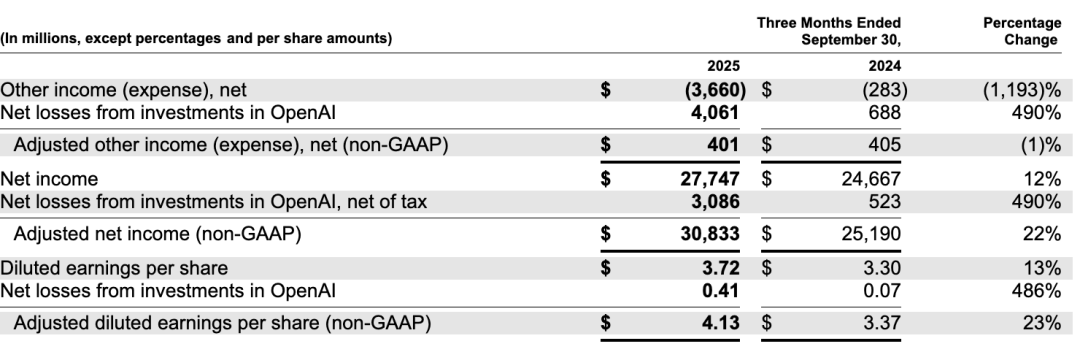

In the third quarter of 2025, Microsoft’s net profit reached $27.7 billion, up 12 percentage points year-over-year.

However, despite earning so much, Microsoft seems a bit “unhappy.”

The gist is: if it weren’t for this “little brother” dragging down performance, profits could have easily broken the $30 billion barrier this quarter!

Net income and EPS for the year were negatively impacted by losses from the investment in OpenAI, reducing them by $3.1 billion and $0.41 per share, respectively.

Wait a minute—didn’t OpenAI recently claim its IPO valuation could reach one trillion dollars?

Logically, Microsoft’s stake should be worth a fortune. So why the loss?

Actually, this isn’t how the accounting works.

On page 9 of the earnings report, Microsoft provided an official explanation:

The investment is accounted for using the equity method. Our share of OpenAI’s income or losses will be reflected in the “Other Income (Expense), Net” line item in our financial statements.

This sentence is crucial, especially the term “equity method,” which conveys significant information.

It means Microsoft cannot simply adjust its book value based on market valuation fluctuations like trading stocks (which would be “mark-to-market accounting”).

Therefore, even if OpenAI’s post-IPO valuation hits $1 trillion, Microsoft cannot add hundreds of billions to its balance sheet overnight.

Conversely, under the equity method, Microsoft’s financial reports are directly tied to OpenAI’s actual operational performance.

Specifically, at each quarterly settlement, Microsoft first looks at how much money OpenAI earned or lost that quarter;

Then, based on its shareholding percentage, it records that portion of profit or loss directly into its own “Other Income/Expense” line item;

In other words, OpenAI’s performance directly impacts Microsoft’s net profit.

The formula might be more intuitive:

This accounting treatment is actually quite common, typically used for investments where the stakeholder holds a significant share but lacks controlling interest.

Once you understand this logic, things get interesting.

Sharp-eyed netizens realized that using Microsoft’s “equity method” calculation, one can reverse-engineer OpenAI’s true financial status from last quarter.

Known: Microsoft reported a $3.1 billion reduction in its financials due to losses from its OpenAI investment;

Also Known: According to disclosures on OpenAI’s organizational restructuring this week, Microsoft currently holds a 27% stake.

A simple arithmetic problem reveals a shocking secret:

OpenAI’s net loss last quarter was $11.5 billion!

Losing So Much and Still IPO?

Upon hearing this big scoop, many netizens who were eagerly awaiting OpenAI’s IPO felt devastated:

They lost $110 billion, yet they want to tell us at the IPO that the company is worth over $1 trillion. Haha…

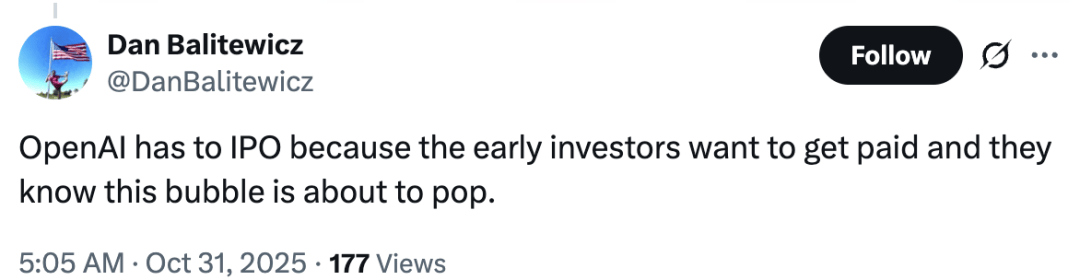

Some netizens even suspect that OpenAI might just be looking to cash out one last time before leaving?

OpenAI must go public as soon as possible because early investors want to cash out and exit. They know this bubble is about to burst.

Ahem, actually, OpenAI isn’t truly “losing” money in the way it sounds.

Yes, the books show a shortfall of over $10 billion, but this doesn’t necessarily indicate problems with their business operations; rather, it reflects the “Prisoner’s Dilemma” facing the entire AI industry today.

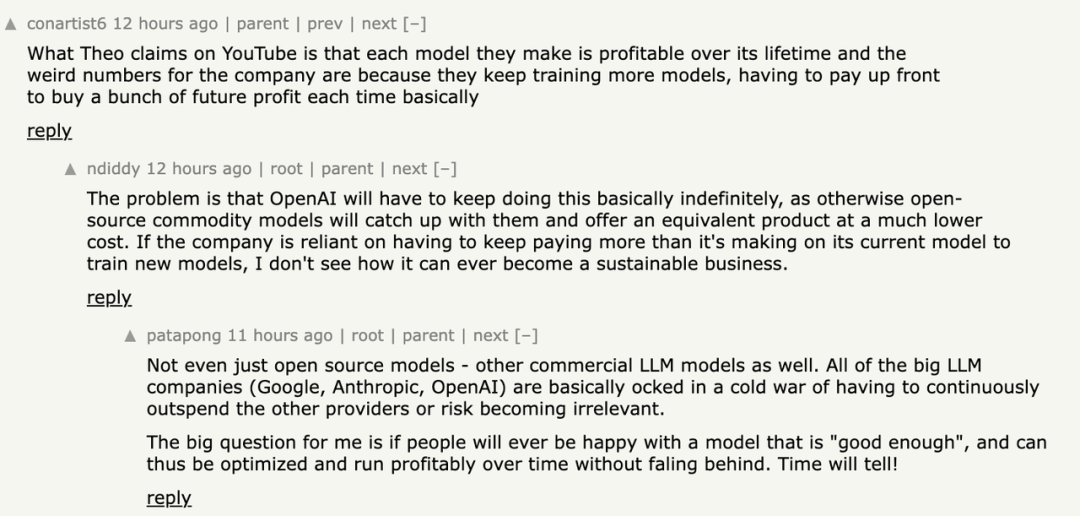

In fact, all AI models released by OpenAI should be profitable throughout their lifecycle.

According to Information, OpenAI’s revenue approximately doubled in the first seven months of this year, reaching an Annualized Run Rate (ARR) of $12 billion.

This means that just from subscriptions and API usage, OpenAI earns roughly $1 billion per month.

Even if model training is incredibly costly, such figures shouldn’t result in an $11.5 billion hole appearing out of thin air.

Netizens pointed out that this money is likely not purely operational costs but mostly R&D expenditures.

The reason for OpenAI’s financial anomaly lies in their continuous training of more models.

The reason for this is that OpenAI must ensure its models remain the State-of-the-Art (SOTA) in the industry at all times.

Otherwise, if open-source models catch up, the flood of free alternatives will instantly overwhelm their commercial empire built on brand recognition.

It’s not just OpenAI; major foundational model companies like Google, Anthropic, and xAI have been drawn into a smokeless “Cold War.”

In the foundational model segment, there is no such thing as user stickiness. If a substitute appears, users will abandon you immediately.

Therefore, they can only keep throwing money at R&D, using compute power and time to maintain their lead—a classic “Prisoner’s Dilemma.”

Thus, although open-source models haven’t visibly taken away the closed-source vendors’ cake, they have exerted immense pressure on these companies’ cost structures through externalities.

However, to be rigorous, OpenAI’s current book “loss” does not mean it is truly losing money.

R&D investment is indeed like a bottomless pit, but from an economic perspective, if revenue covers the “amortized R&D expenses of models under development + daily operational costs,” then OpenAI is not operating at a loss.

After all, the money for R&D and compute has already been spent, and the equipment is running.

As long as OpenAI can recover its variable costs through subscriptions and APIs, there is still reason for the company to keep moving forward.

This is somewhat like a shipping company that borrows from a bank to buy ships for business:

As long as each trip’s freight covers the crew’s wages and fuel costs, even if the cost of buying the ship hasn’t been recovered yet, the business can continue.

Moreover, as long as the ships don’t sink and orders keep coming, there will come a day when the loans are fully repaid, allowing for future cooperation with banks to buy more ships and expand operations.

So, do you think the bank would rush to force them to liquidate assets to repay the money?

By the same logic, Microsoft isn’t currently concerned with whether OpenAI is profitable; what it truly cares about is ensuring its Copilot always has access to the industry’s strongest models.

To keep this ace up its sleeve, Microsoft must continue to pump funds into OpenAI, ensuring it retains top-tier compute power and R&D resources.

Simply put, the relationship between the two is: Microsoft pays for OpenAI’s R&D and computing, while OpenAI focuses on building models, which Microsoft then uses to compete in the enterprise market.

So, although the “little brother” caused the big brother’s book value to drop by $3.1 billion last quarter, this is less a bad debt and more of a strategic subsidy initiated by Microsoft.

Even if it were truly a “mess,” considering Microsoft earned a net profit of $27.7 billion last quarter, losing a mere 3.1 billion is just a drop in the bucket.

Furthermore, the massive compute expenses OpenAI incurs will ultimately flow back into Microsoft’s Azure cloud.

According to the latest cooperation agreement, OpenAI has committed to purchasing an additional $250 billion worth of Azure cloud services in the future.

In summary, Microsoft’s “loss” does not indicate that there is a problem with OpenAI; rather, it demonstrates that—within AI R&D of this scale—subsidies at the infrastructure level have become necessary.

As one netizen put it, the rules of the AI game have long changed: from “who can build the best model” to “who can survive longer while burning cash.”

While Snipe and Clam Struggle, Old Huang Profits

Interestingly, while investors are still arguing heatedly over whether “OpenAI is a bubble,” on another front, Nvidia’s market cap has easily surpassed five trillion dollars.

The current situation can be summarized as: the harder OpenAI loses, the better off “Old Huang” (Jensen Huang) does.

If someone were to ask Jensen Huang how he views OpenAI’s $11.5 billion loss last quarter, Old Huang would probably chuckle inwardly:

Who cares if it’s a bubble? Even if it is, I can refine it into gold.

References

1983947076112412674. 1983947076112412674 — x.com/kimmonismus/status/1983947076112412674